Innovation Corner

Permanent link for Improvise, Adapt, Overcome on April 12, 2024

Entrepreneurs can glean invaluable insights from the Marine Corps Fighting Doctrine's mantra: "Improvise, Adapt, Overcome." In today's dynamic business environment, adaptability is not just beneficial—it's essential. Successful ventures pivot swiftly and innovate to navigate unforeseen challenges.

Improvise

Entrepreneurs often encounter unexpected obstacles that disrupt their plans. As the military adage goes, "No plan survives first contact with the enemy," entrepreneurs must be prepared to deviate from their original strategies. Similar to Marines on the battlefield, they must think creatively, leveraging available resources in unconventional ways to overcome adversity.

Adapt

Adaptability lies at the heart of both military strategy and entrepreneurship. "Slow is smooth, smooth is fast," emphasizing the importance of methodical action even under pressure. In entrepreneurship, staying agile and responsive to changing market dynamics is crucial. Being able to adjust strategies swiftly to new trends and competitive landscapes is key to success.

Overcome

Resilience is paramount in the face of adversity. "Embrace the suck," urging individuals to endure difficult situations without complaint. Entrepreneurs must confront challenges head-on, prioritizing both objectives and the well-being of individuals, as emphasized in "Mission first, people always." By navigating setbacks with determination and grit, entrepreneurs can emerge stronger and more successful.

Conclusion

The Marine Corps mantra illuminates the path to entrepreneurial success. By embracing flexibility, adaptability, and resilience, entrepreneurs can thrive amidst challenges. Channeling the spirit of improvisation, adaptation, and overcoming fosters excellence in entrepreneurship, ensuring ventures not only survive but flourish in the ever-evolving business landscape.

Categories:

entrepreneurship

innovation

management

Posted

by

Thomas Hopper

on

Permanent link for Improvise, Adapt, Overcome on April 12, 2024.

Permanent link for Unveiling the Synergy Between Business Model Canvas and the 4Ps in Product Innovation on March 29, 2024

Two common tools for strategizing and executing business plans are the Business Model Canvas (BMC) and the Marketing Mix, famously known as the 4Ps (Product, Price, Place, and Promotion). While these frameworks are often discussed independently, their overlap can unlock a powerful synergy, enhancing the depth and effectiveness of your business strategy.

The Business Model Canvas, pioneered by Alexander Osterwalder and Yves Pigneur, offers a holistic view of a business model by breaking it down into nine key building blocks: Customer Segments, Value Proposition, Channels, Customer Relationships, Revenue Streams, Key Resources, Key Activities, Key Partnerships, and Cost Structure. This framework serves as a blueprint for understanding how a company intends to create, deliver, and capture value.

The 4Ps framework, introduced by E. Jerome McCarthy, focuses on the essential elements of marketing strategy: Product, Price, Place, and Promotion. It delves into the core components of a marketing plan, guiding businesses in crafting strategies to effectively market their products or services.

While the BMC and the 4Ps might seem distinct at first glance, they converge in several critical areas, particularly concerning product strategy:

-

Product (Part of 4Ps) and Value Proposition (Part of BMC): The product is central to both frameworks. In the 4Ps, product strategy involves decisions regarding product features, branding, and differentiation. Similarly, the Value Proposition block in the BMC encapsulates how a product or service solves a customer's problem or fulfills a need in a unique way. Aligning these two concepts ensures that the product's attributes resonate with the target market's preferences and demands.

-

Price (Part of 4Ps) and Revenue Streams (Part of BMC): Pricing decisions directly impact revenue generation, making the alignment between Price and Revenue Streams crucial. The Price component of the 4Ps framework guides entrepreneurs in setting optimal pricing strategies, considering factors such as costs, competition, and perceived value. Correspondingly, the Revenue Streams block in the BMC outlines how the company monetizes its value proposition. By harmonizing pricing strategies with revenue models, businesses can ensure profitability while delivering value to customers.

-

Place (Part of 4Ps) and Channels (Part of BMC): Place, in the context of the 4Ps, refers to the distribution channels through which products reach consumers. Channels, a key element of the BMC, delineate how a company delivers its value proposition to customers. Integrating these concepts involves selecting the most suitable distribution channels to reach target customers efficiently. Whether through direct sales, online platforms, or intermediaries, aligning Place with Channels optimizes the product's accessibility and enhances the overall customer experience.

-

Promotion (Part of 4Ps) and Customer Relationships (Part of BMC): Promotion encompasses marketing communications activities aimed at raising awareness and driving sales. On the BMC, Customer Relationships elucidate how a company interacts with its customers to cultivate loyalty and satisfaction. By aligning promotional efforts with the desired type of customer relationships (e.g., personal assistance, self-service), businesses can tailor their marketing campaigns to effectively engage with their target audience, fostering long-term relationships and brand advocacy.

In essence, while the Business Model Canvas provides a comprehensive framework for mapping out the various components of a business model, the 4Ps framework offers a focused lens on marketing strategy. By recognizing their intersections and aligning the relevant elements, entrepreneurs can craft cohesive and robust business strategies that resonate with customers, drive value creation, and fuel sustainable growth. Embracing this synergy empowers innovators to navigate the complexities of product innovation and entrepreneurship with clarity and purpose.

Categories:

entrepreneurship

innovation

marketing

Posted

by

Thomas Hopper

on

Permanent link for Unveiling the Synergy Between Business Model Canvas and the 4Ps in Product Innovation on March 29, 2024.

Permanent link for How to Price Your Product: Understanding the Difference Between Price and Cost on March 8, 2024

Understanding Product Pricing: Navigating the Price vs. Cost Conundrum

As entrepreneurs and intrepreneurs venture into the world of product development, they inevitably encounter the question: "How much does it cost?" This seemingly simple query actually warrants a deeper understanding, as it involves distinguishing between price—what the customer pays—and cost—what it takes for you to deliver the product to the customer's hands. Moreover, it's essential to differentiate between current costs and those at scale.

1. Addressing Customer Inquiries: The Price Perspective

When engaging with potential customers, particularly those eager to make a purchase, their primary concern revolves around the immediate price. For them, the question translates to, "What's the price, right now?" It's imperative to have a response ready to validate the market and encourage sales. Initially, pricing should focus on market testing rather than operational efficiency. Aim for a premium price point to gauge market receptivity, keeping in mind that early pricing need not correlate with actual costs.

2. Meeting Investor and Stakeholder Expectations: The Cost at Volume

Conversations with investors or internal stakeholders typically revolve around the cost at volume. While estimating costs at scale may seem daunting, it's feasible with a strategic approach. Rather than pinpointing exact costs for every component, identify the key cost drivers and approximate their expenses at the highest feasible volume. For instance, if you're envisioning mass production of a smartphone, aim for a volume estimate that aligns with market demand while remaining realistic.

3. Illustrating Cost Dynamics: A Practical Example

Consider the scenario of manufacturing smartphones in China and shipping them to the U.S. west coast. Initially, shipping costs per phone may be significant. However, as volumes increase, economies of scale come into play, driving down the per-unit shipping cost substantially. Such insights allow you to provide stakeholders with informed estimates, demonstrating the potential cost reductions at scale.

4. Embracing the Cost-Volume Relationship

The relationship between cost and volume applies universally across products and services. As your operations scale, variable costs become increasingly dominant, leading to lower per-unit expenses. This dynamic underscores the importance of targeting high-value customer segments early on, prioritizing premium pricing over cost-conscious mass markets.

5. Navigating Market Opportunities

While high-value customer segments are often the initial focus for startups, exceptions exist. Certain market opportunities may lie in cost-conscious segments, where underserved customers seek affordable alternatives. By offering lower-margin substitutes with strategic feature adjustments, startups can carve out a niche and gain market share.

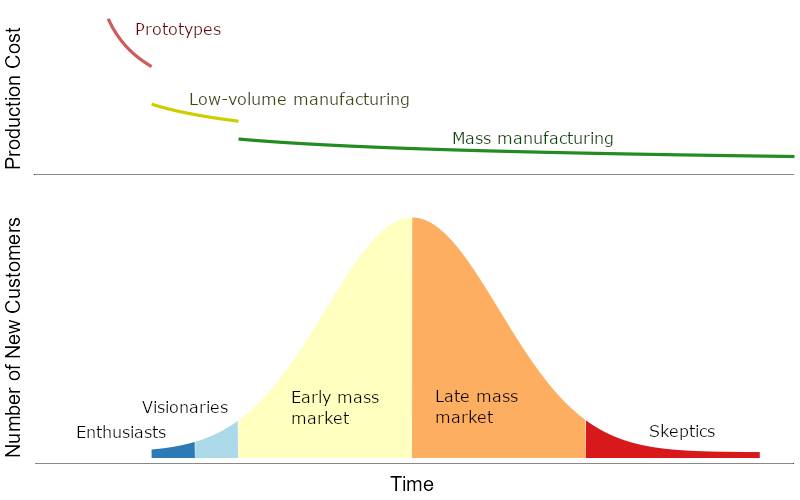

In conclusion, mastering the interplay between price and cost is essential for entrepreneurial success. By understanding customer expectations, investor perspectives, and cost dynamics, startups can navigate pricing challenges effectively, paving the way for sustainable growth and profitability.

Production costs decrease over time, while market adoption increases, slows, then falls off as markets become saturated and alternatives take over. Which customer group you're talking to will determine which cost model you're using.

Categories:

entrepreneurship

innovation

management

marketing

Posted

by

Thomas Hopper

on

Permanent link for How to Price Your Product: Understanding the Difference Between Price and Cost on March 8, 2024.

Permanent link for Maximizing Market Potential: A Guide for First-Time Entrepreneurs on March 1, 2024

Are you diving into entrepreneurship for the first time, eager to develop a new product or service? Amidst the excitement, it's crucial to understand market dynamics to unlock your venture's true potential. Let's explore how you can navigate market potential effectively and pave the way for sustainable growth.

Understanding Market Segmentation: Demystifying TAM, SAM, and SOM

Picture yourself pioneering an innovative inventory management solution tailored for businesses. Your Total Addressable Market (TAM) isn't the entire business landscape but specifically the portion of businesses that could benefit from your solution.

Moving forward, your Serviceable Addressable Market (SAM) is a subset of TAM, representing the portion of businesses within TAM that you can effectively target and serve based on your unique value proposition and business model.

Finally, your Serviceable Obtainable Market (SOM) is the realistic fraction of SAM that you expect to capture as actual sales. This figure evolves over time with strategic adjustments and resource allocation.

Strategies for Sustainable Growth: Realism Over Aspiration

Prioritize bottom-up estimations and realistic projections over lofty aspirations of quick exits. Building a solid foundation and catering to a niche market are your pathways to long-term success and sustainable growth. Remember, success isn't solely about exit magnitude but impact and longevity in the market.

Embracing the Entrepreneurial Journey: Final Thoughts

Navigate market potential with optimism and resilience, viewing challenges as opportunities for growth. By staying true to your vision and executing with precision, you lay the groundwork for a successful venture. Ready to maximize your venture's potential? Let's embark on this journey together.

Unlock Your Venture's Potential Today

Ready to unlock your venture's true revenue potential? Begin by understanding market dynamics and refining your strategies for sustainable growth. Stay focused on your journey and embrace every milestone along the way.

Let's turn your entrepreneurial vision into reality. Reach out to explore how you can optimize market potential for your venture.

Techcrunch has some great advice and insight: Nice try, startup, but that's not your serviceable obtainable market (SOM)

Categories:

entrepreneurship

marketing

Posted

by

Thomas Hopper

on

Permanent link for Maximizing Market Potential: A Guide for First-Time Entrepreneurs on March 1, 2024.

Permanent link for Innovation on February 9, 2024

In today's fast-paced business landscape, the key to success often lies in the ability to innovate quickly and bring products to market faster than the competition. For businesses striving for relevance and growth, an efficient innovation process is not just a luxury; it's a necessity. In this blog, we'll explore strategic approaches and practical tips to help you streamline your innovation process and ensure that your product reaches the market swiftly and successfully.

- Start with a Clear Vision

Before embarking on the innovation journey, it's crucial to have a clear vision of what problem your product solves and who your target audience is. Define your value proposition and ensure that it aligns with market needs. A well-defined vision serves as a guiding light, helping your team stay focused and make informed decisions throughout the development process.

- Embrace Agile Methodology

Agile methodology has become synonymous with rapid innovation. By breaking down the development process into smaller, manageable tasks and regularly reassessing priorities, you can adapt to changes swiftly. This iterative approach allows for continuous improvement, reducing the risk of late-stage changes that could delay your time to market.

- Foster a Culture of Innovation

Innovation is not solely the responsibility of the R&D department; it should be ingrained in the entire organizational culture. Encourage cross-functional collaboration, reward creative thinking, and create an environment where employees feel empowered to share their ideas. A culture of innovation promotes a collective mindset that can significantly speed up the product development process.

- Conduct Rapid Prototyping

Waiting until the final stages to test your product can be a costly mistake. Rapid prototyping allows you to gather valuable feedback early in the process, enabling you to make necessary adjustments swiftly. By incorporating user feedback throughout development, you reduce the likelihood of major overhauls later on, saving both time and resources.

- Utilize Technology and Automation

Leverage technology to automate repetitive tasks, streamline workflows, and enhance collaboration. Project management tools, communication platforms, and collaborative software can significantly increase efficiency. Automation not only accelerates processes but also minimizes the risk of human error, ensuring that your product development stays on track.

- Build Strategic Partnerships

Collaborating with external partners can provide access to valuable resources and expertise, accelerating the development process. Whether it's forming strategic alliances, outsourcing specific tasks, or leveraging existing networks, partnerships can help you overcome challenges and bring your product to market faster.

- Prioritize Minimal Viable Product (MVP)

Instead of waiting for a fully polished product, focus on delivering a Minimal Viable Product (MVP) that addresses the core needs of your target audience. Launching an MVP allows you to gather real-world feedback, validate assumptions, and make necessary adjustments before investing in extensive features. This approach not only accelerates time to market but also reduces the risk of building a product that misses the mark.

To borrow from management guru Peter Drucker, businesses have only two core functions, and innovation is one of them. By incorporating these strategies into your innovation process, you can position your business as a dynamic force in your industry, delivering products to market faster and staying ahead of the competition. Remember, the key lies not only in developing groundbreaking ideas but also in executing them swiftly and efficiently. Embrace innovation, foster a culture of agility, and watch your business thrive in the ever-evolving landscape of today's market.

Categories:

entrepreneurship

innovation

management

Posted

by

Thomas Hopper

on

Permanent link for Innovation on February 9, 2024.

Permanent link for Why Startups Fail (and what you can do about it) on January 19, 2024

New product and service launches fail for many reasons. When the company is a startup, it's not just the product or service that fails, but the whole company. If you know what to watch out for, though, you can greatly increase your chances of success.

One of the main reasons that founders give is insufficient funding; that they run out of cash. This is often the last problem that a startup faces before shuttering, but it's almost always a symptom of deeper problems.

There have been multiple studies on this, such as this Harvard study, published in 2021, and CB Insights' separate study, also published in 2021. Both studies found that the top reasons for failure include

- No market need, also described as insufficient customer discovery and demand validation;

- Not having the right team, generally as a result of lacking industry experience;

- Poor planning and execution, usually encountered as either over-optimistic plans or as the adoption of strategies that lead to higher cash burn rates than can be absorbed by available funding.

What can you do to bolster your chances of success

- Study and understand your target customers;

- Clearly define the problem you are solving for them in terms they have expressed;

- Validate demand for a solution;

- Build a founding team with both the right attitudes (the willingness to learn and to work in multiple rolls) and the right experience;

- Know your financials and plan for sustainable both development and growth.

StartupGrind has more good advice.

Categories:

entrepreneurship

management

Posted

by

Thomas Hopper

on

Permanent link for Why Startups Fail (and what you can do about it) on January 19, 2024.

Permanent link for Build Your MVP on January 5, 2024

Launching a new product is an exhilarating journey that demands careful planning, strategic thinking, and a deep understanding of your target audience. To fully understand your target audience, you have to put product in their hands. Rather than spending time and money building the better mousetrap, it's best to start with the creation of a Minimum Viable Product (MVP), a crucial step that can make or break your venture. How do you build a winning MVP?

-

Define Your Core Value Proposition: Before diving into development, it's essential to clearly define your product's core value proposition. What problem does it solve? How does it meet the needs of your target audience? The answers to these questions will guide the development of your MVP and ensure it addresses the most critical aspects of your product.

-

Identify Key Features: An MVP is not about including every possible feature but about focusing on the essential functionalities that demonstrate the product's value. Identify the features that directly contribute to solving the core problem. This laser focus ensures a quicker development process and allows you to gather valuable feedback sooner.

-

Keep It Simple and User-Friendly: Simplicity is key when creating an MVP. A clean and intuitive user experience not only attracts users but also allows them to understand and use your product effortlessly. Avoid unnecessary complexities, and prioritize a seamless user experience to encourage user engagement.

-

Build Rapid Prototypes: Prototyping is a powerful tool in the MVP development process. Rapid prototypes act as a tangible representation of your product, helping you identify potential issues early on and to iterate quickly as you learn what works and what does not.

-

Embrace Iterative Development: The MVP is not a one-time effort but a process of continuous improvement. Embrace an iterative development approach, releasing small updates and improvements based on user feedback. This not only keeps your product aligned with user needs but also demonstrates a commitment to ongoing enhancement. The frequency of updates and amount of development that goes into each iteration will depend critically the economics of developing, producing and testing prototypes.

-

Collect User Feedback: User feedback is the lifeblood of a successful MVP. Release your product to a select group of users, gather their feedback, and use it to refine and enhance your offering. Leverage feedback loops to continuously optimize your product based on real-world user experiences.

-

Measure and Analyze: Implement analytics tools to track user behavior and engagement. This data provides valuable insights into how users interact with your product, allowing you to make data-driven decisions. Metrics such as user retention, conversion rates, and user satisfaction are crucial indicators of your MVP's success.

-

Prepare for Scalability: While the focus is on building a minimum viable product, it's crucial to plan for scalability. Choose a robust architecture that can grow with your user base. Anticipate potential challenges associated with increased demand and have a roadmap for scaling your infrastructure accordingly.

Building a Minimum Viable Product is an exciting and transformative phase in the product development journey. By staying focused on your core value proposition, embracing simplicity, iterating based on user feedback, and planning for scalability, you set the foundation for a successful product launch. Remember, the MVP is not the end but the beginning of a journey toward creating a product that truly meets the needs of your audience.

Categories:

entrepreneurship

innovation

Posted

on

Permanent link for Build Your MVP on January 5, 2024.

Permanent link for Boost Your Small Business Success on December 15, 2023

Starting a small, bootstrapped business is no small feat, and ensuring consistent quality in your products or services is crucial for long-term success. One effective way to achieve this is by incorporating elements of the ISO 9001 standard into your business processes. ISO 9001 is an internationally recognized quality management standard that can guide you to developing better, more consistent business processes, delivering better and more consistent results to your customers. Here are some practical tips for small business owners to implement key aspects of ISO 9001.

- Understand Customer Needs and Expectations:

ISO 9001 emphasizes a customer-centric approach. Start by clearly understanding your customers' needs and expectations. Engage with them through surveys, feedback forms, and social media to gather valuable insights. Use this information to tailor your products or services to meet their requirements more effectively.

- Establish a Quality Policy:

Define a quality policy that aligns with your business objectives. Clearly communicate this policy to your team and ensure everyone understands their role in maintaining quality. A well-defined quality policy provides a framework for decision-making and helps in consistently delivering high-quality outcomes.

- Implement Documented Processes:

Documenting your processes is a fundamental step in ISO 9001. Create clear, step-by-step procedures for key business activities, such as product development, customer service, and order fulfillment. This documentation serves as a reference for employees and helps maintain consistency, especially as your business grows.

- Set and Monitor Key Performance Indicators (KPIs):

Identify key performance indicators that align with your business goals and customer expectations. Regularly monitor these KPIs to track your business's performance and identify areas for improvement. This data-driven approach will enable you to make informed decisions and continuously enhance your processes.

- Train and Empower Your Team:

Invest in training programs to ensure that your team understands the importance of quality and is equipped with the necessary skills to meet customer expectations. Empower employees to take ownership of their roles and contribute to the overall quality objectives of the business.

- Regularly Conduct Internal Audits:

Internal audits are a proactive way to identify potential issues and ensure compliance with established processes. Regularly review your documented procedures and conduct internal audits to identify areas for improvement. This continuous improvement cycle is integral to the ISO 9001 framework.

- Encourage a Culture of Continuous Improvement:

Foster a culture of continuous improvement within your organization. Encourage employees to suggest improvements and innovations in processes. Implement a feedback loop that allows for the timely review and incorporation of valuable suggestions, leading to a more agile and adaptive business.

Conclusion:

Implementing ISO 9001 principles in your small, bootstrapped business can be a game-changer. By focusing on customer needs, documenting processes, monitoring performance, and fostering a culture of continuous improvement, you can deliver better, more consistent results to your customers. ISO 9001 is not just a certification; it's a mindset that can help your business thrive in a competitive landscape while building a reputation for excellence. Embrace these tips, and watch your small business grow with a commitment to quality.

Categories:

entrepreneurship

management

Posted

by

Thomas Hopper

on

Permanent link for Boost Your Small Business Success on December 15, 2023.

Permanent link for Marketing on a Budget on December 8, 2023

Marketing on a budget might sound challenging, but with creativity and strategic thinking, you can make a big impact without breaking the bank. Here are 10 budget-friendly marketing strategies to help your small business thrive:

1. Leverage Social Media Power:

Create engaging profiles on popular social media platforms like Facebook, Instagram, and Twitter. Share behind-the-scenes glimpses, customer testimonials, and promotions. Engage with your audience by responding to comments and messages promptly.

2. Start a Blog:

Share your expertise and passion through a blog on your website. Write informative and entertaining posts related to your industry, products, or local community. This not only establishes you as an authority but also improves your website's search engine ranking.

3. Local Collaborations:

Partner with other local businesses for cross-promotions. You can share each other's products or services on social media, collaborate on events, or even offer joint discounts to customers.

4. DIY Public Relations:

Reach out to local newspapers, magazines, and online publications. Offer them a compelling story about your business, emphasizing what makes you unique. Local media is often looking for interesting content about businesses in the community.

5. Customer Referral Programs:

Encourage your existing customers to refer friends and family by offering them discounts or freebies for every successful referral. Word of mouth is a powerful tool, and happy customers can be your best advocates.

6. Create Engaging Visual Content:

Invest time in creating visually appealing content. Use free tools like Canva to design eye-catching graphics for social media posts, promotional materials, and your website.

7. Host Events and Workshops:

Organize local events or workshops related to your business. This could be a product launch, a how-to session, or a community gathering. Events create buzz and give people a reason to visit your store.

8. Email Marketing:

Build an email list and regularly send out newsletters with updates, promotions, and exclusive offers. Email marketing is a cost-effective way to stay connected with your audience and drive repeat business.

9. Optimize Your Google My Business Listing:

Ensure your business information is accurate and up-to-date on Google My Business. This helps local customers find you easily and provides essential details about your business.

10. Harness the Power of User-Generated Content:

Encourage customers to share their experiences with your products or services on social media. Repost user-generated content on your platforms to build trust and showcase the real value your business brings.

Remember, marketing is an ongoing process. Be consistent, monitor the results of your efforts, and adjust your strategies accordingly. With a bit of creativity and dedication, your mom-and-pop business can stand out in a crowded market without burning a hole in your pocket. Good luck!

Categories:

entrepreneurship

marketing

Posted

by

Thomas Hopper

on

Permanent link for Marketing on a Budget on December 8, 2023.

Permanent link for Doing Market Research on December 1, 2023

Market research is a crucial step in starting your business. By understanding your target customers, your competitors, and the current market landscape, you can ensure better market adoption and higher value.

Here are a few specific ways you can conduct market research:

Surveys: Surveys are an easy way to gather information from a large number of people quickly and inexpensively. You can use a tool like Google Forms or SurveyMonkey to create and distribute a survey to gather insights about your target audience, their needs, and their preferences. Be careful, though, how you write questions to avoid leading your respondents to give you the answers you like rather than solid data.

Focus groups: A focus group is a small, representative group of people who are brought together to discuss and provide feedback on a particular topic or product. You can use a focus group to gather in-depth insights and opinions about your business or product. Small Business Trends offers some more in-depth advice on How to Conduct a Focus Group.

Industry data analysis: There are many sources of industry data that can help you understand trends and patterns in your market. This can include data from trade associations, government agencies, or market research firms. The SBA provides links to some great databases and other tools for market research and competitive analysis.

Customer interviews: Conducting in-depth interviews with current or potential customers can provide valuable insights into their needs, motivations, and decision-making processes. You can use these interviews to gather specific feedback and ideas for improving your products or marketing efforts. More detailed advice can be found in the article Customer Discovery Interviews: A Secret of Successful Startups.

Competitor analysis: Analyzing your competitors can help you understand their strengths and weaknesses, and identify areas where you can differentiate your business. This can include things like reviewing their website and social media accounts, analyzing their product offerings, and gathering customer feedback about their products or services. Here are 5 Outstanding Competitor Analysis Tools for Startups.

Your regional Small Business Development Center will probably be able to help you conduct market research free of charge, and many local libraries provide access to demographic databases that can be used to gauge market size or build potential customer lists, like the Gale Business Demographics Now database and ReferenceGuru's AtoZ Databases.

Categories:

entrepreneurship

marketing

Posted

by

Thomas Hopper

on

Permanent link for Doing Market Research on December 1, 2023.