Innovation Corner

Permanent link for Words of Wisdom for Entrepreneurs on June 28, 2025

In the fast-paced, ever-evolving world of business, timeless principles can offer clarity and direction. Ancient wisdom, from Sun Tzu’s strategies in The Art of War to the U.S. Navy SEALs’ philosophy of “slow is smooth, smooth is fast,” provides a valuable toolkit for entrepreneurs seeking sustainable success. Here’s how age-old advice can translate into practical strategies for business management today.

1. Know Your Enemy and Know Yourself

One of the most widely cited principles in business, derived from Sun Tzu’s The Art of War, is: “If you know the enemy and know yourself, you need not fear the result of a hundred battles.” (source). In today’s terms, “enemy” might be your competitors, the market forces, or even internal challenges within your own business.

Knowing your enemy involves thorough competitive analysis. By studying your competitors' strengths and weaknesses, you can identify opportunities for differentiation. Equally important, however, is self-awareness. As an entrepreneur, understanding your own strengths, weaknesses, and tendencies allows you to make informed decisions and leverage your unique skills. Self-awareness fosters resilience, especially when unexpected challenges arise, and enhances your ability to capitalize on opportunities where competitors may falter.

2. Slow is Smooth, Smooth is Fast

The Navy SEAL mantra, “Slow is smooth, smooth is fast” (source), is particularly relevant for entrepreneurs who feel pressured to move quickly to capture market share. The phrase advises a careful, measured approach, one that prioritizes precision over speed. In business, rushing can lead to costly mistakes and missteps. Instead, taking the time to establish efficient systems and quality processes enables smoother, faster execution in the long run.

By adopting this mindset, entrepreneurs can reduce errors, save resources, and ultimately accelerate their path to growth. For instance, rather than rushing to launch a new product, spend time refining it and ensuring it meets market demands. When the product is ready, its quality and market fit will contribute more to its success than speed ever could.

3. "First, Seek to Understand, Then to Be Understood" – Stephen Covey

Though not ancient, Stephen Covey’s principle from The 7 Habits of Highly Effective People is rooted in classical wisdom. Covey emphasizes that listening and understanding others’ perspectives should come before asserting your own. In business, this applies not only to negotiations but also to client relations and employee management. Prioritizing understanding fosters trust, builds stronger relationships, and lays the groundwork for more effective communication and collaboration. By listening first, entrepreneurs can tailor solutions to actual needs and better align their offerings with customer expectations.

4. "Divide and Conquer" – Julius Caesar

The Roman general Julius Caesar applied “divide and conquer” to warfare, but the principle is equally effective in marketing strategy, particularly in market segmentation. When applied to business, "divide and conquer" means segmenting a broad market into smaller, well-defined groups of customers with specific needs. Instead of trying to serve the entire market with a single approach, entrepreneurs can focus on one or more niche segments, customizing their strategies to resonate with each group.

For example, if a tech entrepreneur is introducing a new productivity app, they might initially target two segments: remote workers and freelancers, tailoring messaging and features to each group's unique needs. By understanding each segment’s challenges—such as work-life balance for remote workers or time management for freelancers—the business can more effectively allocate resources, improve marketing efficiency, and build brand loyalty within each niche before expanding further.

In Conclusion: The Practicality of Ancient Wisdom

Ancient principles continue to hold relevance in today’s entrepreneurial world, from knowing your market and your own capabilities to approaching growth with deliberate, strategic steps. Embracing this wisdom allows entrepreneurs to cultivate discipline, resilience, and insight that drive long-term success. As these age-old insights remind us, sometimes the most effective strategies are those proven through centuries of application.

If you want to dive deeper into these sources, you can explore The Art of War on Goodreads and the SEAL principles on Military.com.

Categories:

entrepreneurship

innovation

management

Posted

by

Thomas Hopper

on

Permanent link for Words of Wisdom for Entrepreneurs on June 28, 2025.

Permanent link for Funding Your Business Growth (DRAFT) on March 8, 2025

https://www.entrepreneur.com/money-finance/how-to-find-the-right-balance-of-debt-to-grow-your-business/439948

https://hbr.org/1982/07/how-much-debt-is-right-for-your-company

https://www.uschamber.com/co/run/finance/good-vs-bad-debt-for-small-business

https://www.lendingtree.com/business/debt-schedule/

Coverage ratio

EBITDA/debt >= 2.0

Current cash flow & projected cash flow

Categories:

entrepreneurship

management

Posted

by

Thomas Hopper

on

Permanent link for Funding Your Business Growth (DRAFT) on March 8, 2025.

Permanent link for Market Segments? Customer Segments? (DRAFT) on March 8, 2025

https://www.perceptive.co.nz/blog/difference-between-market-segmentation-target-audience-customer-segmentation-and-personas

Posted by Thomas Hopper on Permanent link for Market Segments? Customer Segments? (DRAFT) on March 8, 2025.

Permanent link for How to Find a Business Idea That's Actually Worth Pursuing (DRAFT) on March 8, 2025

Not all business ideas are successful; according to the U.S. Bureau of Labor Statistics, nearly half of all new businesses fail

https://www.entrepreneur.com/starting-a-business/is-your-business-idea-worth-pursuing-heres-how-to-tell/438738

Categories:

entrepreneurship

Posted

by

Thomas Hopper

on

Permanent link for How to Find a Business Idea That's Actually Worth Pursuing (DRAFT) on March 8, 2025.

Permanent link for Innovation? (DRAFT) on January 31, 2025

"Innovation" is a fuzzy term. All too often, it's just a buzzword. We know innovation when we see it, but how do we describe it? Is it coming up with a new idea? Doing something better?

I like to think about innovation as the process of transforming an idea for a superior, less-costly product (or service) into a commercial offering. It's the series of steps (and mis-steps) needed to go from concept to a refined offering that other people will spend their money on. By thinking of innovation as a process, I find it's easier to identify what activities need to be completed and when we need to start on them.

It can also make innovation more accessible by demystifying

Categories:

innovation

Posted

by

Thomas Hopper

on

Permanent link for Innovation? (DRAFT) on January 31, 2025.

Permanent link for How Lean Start-Up Principles Can Empower Startups on November 1, 2024

Starting a lifestyle business—whether a local consultancy, an online boutique, or a service-based venture—presents unique challenges. Many founders invest significant time and resources before discovering whether their product or service truly meets customer needs. This is where the lean start-up methodology can help lifestyle entrepreneurs build a sustainable, customer-focused business while avoiding unnecessary costs and complexity.

What is the Lean Start-Up Method?

The lean start-up approach shifts focus from detailed business planning to an agile, flexible model built on direct customer feedback. By creating a "minimum viable product" (MVP) and listening closely to early customers, lifestyle entrepreneurs can refine their business offerings and quickly address what works and what doesn’t. Though lean start-up principles are often associated with high-growth tech ventures, they offer particular value for lifestyle businesses by emphasizing a practical, customer-centered development process.

Why Lean Start-Up Works for Lifestyle Businesses

- Direct Customer Input: Rather than investing heavily in features or services based on assumptions, lean start-ups focus on learning from real customers from day one. This approach allows lifestyle business owners to create products that address genuine needs, improving customer satisfaction and retention.

- Flexible and Affordable Model: Lean start-ups use tools like the “business model canvas” to outline hypotheses about their customers and market. As these assumptions are tested, entrepreneurs can make informed decisions without committing substantial resources to a static business plan.

- Efficient Time and Cost Management: By focusing on MVPs and rapid iteration, lean methods help lifestyle entrepreneurs get to market faster with lower upfront costs. This approach is particularly beneficial for businesses with limited resources, ensuring they remain financially nimble and adaptable as the business grows.

Embracing Lean for a Sustainable Lifestyle Business

Incorporating lean principles offers lifestyle business owners the advantage of flexibility, lower risk, and a better fit with customer expectations. By prioritizing experimentation, learning, and agility, lifestyle entrepreneurs can create businesses that are not only sustainable but also responsive to changing customer demands. Adopting lean start-up practices doesn’t mean sacrificing quality; rather, it empowers entrepreneurs to deliver more targeted value to their customers while building a business aligned with their goals and lifestyle.

Steve Blank, the guru of Lean Startup, has more for you at Harvard Business Review.

Categories:

entrepreneurship

innovation

Posted

by

Thomas Hopper

on

Permanent link for How Lean Start-Up Principles Can Empower Startups on November 1, 2024.

Permanent link for Decision Tools for Entrepreneurs on May 3, 2024

Making smart decisions is crucial for your business's success. In this post, I'll introduce you to easy-to-use tools that can help you make better choices confidently.

-

Decision Trees : Picture a tree with branches showing different choices and their possible outcomes. Decision trees help you see the consequences of each decision. To create one, start by listing your options. Then, map out what might happen for each option. Assign probabilities based on what you know or estimate. This visual aid makes it easier to choose the best path forward.

-

Pareto Analysis : Ever heard of the 80/20 rule? It says that 80% of your results come from 20% of your efforts. Pareto analysis helps you focus on what matters most. List your tasks or problems, then identify which ones have the biggest impact. By tackling these first, you'll maximize your efforts for success.

-

SWOT Analysis : SWOT stands for strengths, weaknesses, opportunities, and threats. This tool helps you understand your business better. Make a list for each category. Your strengths and weaknesses are internal, while opportunities and threats are external. By knowing these, you can plan smarter strategies.

Here's how to use it: List your business's strengths, like unique products or talented team members. Then, jot down weaknesses, such as limited resources or inexperienced staff. Next, identify opportunities in the market, like growing demand for your product. Finally, consider threats, like new competitors or changing regulations. With this insight, you can focus on leveraging strengths, improving weaknesses, seizing opportunities, and mitigating threats.

-

Decision Matrices : Imagine a table with options listed on one side and criteria on the other. Decision matrices help you compare choices objectively. Start by listing your options and criteria. Assign weights to criteria based on importance, then rate each option on how well it meets each criterion. Multiply the ratings by the weights and add them up. The option with the highest score is likely your best choice.

Let's say you're choosing between different suppliers for a critical component. Your criteria might include cost, quality, reliability, and delivery time. Assign weights based on what matters most to your business. Then, rate each supplier on each criterion. Multiply the ratings by the weights and add them up for each supplier. The one with the highest total score is your top pick.

The Eisenhower Matrix is similar to a decision matrix, and can be especially useful for prioritizing your activities.

-

Cost-Benefit Analysis : This tool helps you decide if a choice is worth it financially. List all costs and benefits associated with a decision. Compare them to see if benefits outweigh costs. If they do, it's probably a good move for your business.

Here's how it works: Let's say you're considering investing in new equipment. List all costs, including purchase price, installation, and maintenance. Then, list benefits like increased productivity or reduced downtime. Quantify these benefits in monetary terms if possible. Finally, compare total costs to total benefits. If benefits outweigh costs, the investment is likely to pay off.

-

Expected Monetary Value (EMV): Expected Monetary Value is a statistical technique used to assess the potential value of different outcomes based on their probabilities. By multiplying the probability of each outcome by its associated monetary value and summing the results, entrepreneurs can calculate the expected value of a decision or project. EMV complements the other tools, and works especially well with decision trees and cost-benefit analysis.

To apply EMV, start by identifying the possible outcomes of a decision or project and estimating their probabilities. Then, assign a monetary value to each outcome, representing its potential impact on revenue, cost savings, or other financial metrics. Multiply the probability of each outcome by its monetary value and sum the results to calculate the expected monetary value. This provides entrepreneurs with a quantitative measure of the potential value of different options, helping them prioritize and make informed decisions.

These tools can make decision-making less daunting for business owners and managers. By using decision trees, Pareto analysis, SWOT analysis, decision matrices, and cost-benefit analysis, you can make informed decisions confidently. Remember, successful decision-making also requires critical thinking and creativity. Embrace your journey with confidence!

Categories:

management

Posted

by

Thomas Hopper

on

Permanent link for Decision Tools for Entrepreneurs on May 3, 2024.

Permanent link for Improvise, Adapt, Overcome on April 12, 2024

Entrepreneurs can glean invaluable insights from the Marine Corps Fighting Doctrine's mantra: "Improvise, Adapt, Overcome." In today's dynamic business environment, adaptability is not just beneficial—it's essential. Successful ventures pivot swiftly and innovate to navigate unforeseen challenges.

Improvise

Entrepreneurs often encounter unexpected obstacles that disrupt their plans. As the military adage goes, "No plan survives first contact with the enemy," entrepreneurs must be prepared to deviate from their original strategies. Similar to Marines on the battlefield, they must think creatively, leveraging available resources in unconventional ways to overcome adversity.

Adapt

Adaptability lies at the heart of both military strategy and entrepreneurship. "Slow is smooth, smooth is fast," emphasizing the importance of methodical action even under pressure. In entrepreneurship, staying agile and responsive to changing market dynamics is crucial. Being able to adjust strategies swiftly to new trends and competitive landscapes is key to success.

Overcome

Resilience is paramount in the face of adversity. "Embrace the suck," urging individuals to endure difficult situations without complaint. Entrepreneurs must confront challenges head-on, prioritizing both objectives and the well-being of individuals, as emphasized in "Mission first, people always." By navigating setbacks with determination and grit, entrepreneurs can emerge stronger and more successful.

Conclusion

The Marine Corps mantra illuminates the path to entrepreneurial success. By embracing flexibility, adaptability, and resilience, entrepreneurs can thrive amidst challenges. Channeling the spirit of improvisation, adaptation, and overcoming fosters excellence in entrepreneurship, ensuring ventures not only survive but flourish in the ever-evolving business landscape.

Categories:

entrepreneurship

innovation

management

Posted

by

Thomas Hopper

on

Permanent link for Improvise, Adapt, Overcome on April 12, 2024.

Permanent link for Mastering the Fail-Fast Approach: A Blueprint for Entrepreneurial Success on April 5, 2024

Throughout my career, I've focused on developing cutting-edge technologies and products. One of the most influential figures I've worked with, a brilliant scientist, introduced me to the concept of "fail fast."

Previously, my approach revolved around testing various inventive ideas and assessing their viability. As a team, we aimed to replicate successful outcomes and iterate on new concepts.

While we experienced some successes, we also encountered numerous failures, some of which were avoidable and overshadowed our achievements. Failure can come with significant costs.

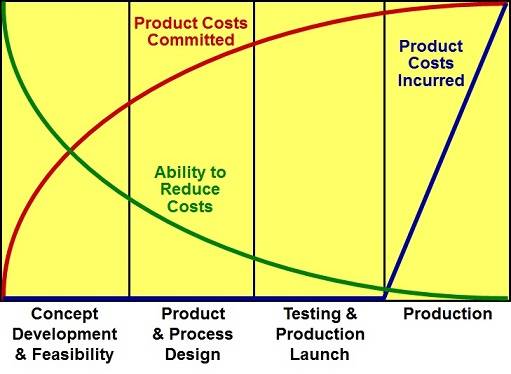

As we progress towards market launch, flexibility decreases, and changes become more expensive. Simultaneously, development expenses escalate, making it crucial to identify and address potential flaws early on to minimize costs.

The fail-fast mindset acknowledges that no idea is perfect and seeks to identify weaknesses swiftly and efficiently. Rather than focusing solely on success, the emphasis is on identifying and mitigating failure points.

To implement this approach, it's essential to define clear hypotheses and develop a comprehensive test plan. For example, testing different website designs through A/B testing to determine their impact on conversion rates.

By embracing the fail-fast approach, entrepreneurs can quickly learn from mistakes and make necessary improvements. Failure becomes an opportunity for growth rather than a setback.

When developing new products or services, the costs spent on development increases, while the flexibility in making changes to the design of the product or service decreases. Image from NPD Solutions.

Categories:

innovation

management

Posted

by

Thomas Hopper

on

Permanent link for Mastering the Fail-Fast Approach: A Blueprint for Entrepreneurial Success on April 5, 2024.

Permanent link for Unveiling the Synergy Between Business Model Canvas and the 4Ps in Product Innovation on March 29, 2024

Two common tools for strategizing and executing business plans are the Business Model Canvas (BMC) and the Marketing Mix, famously known as the 4Ps (Product, Price, Place, and Promotion). While these frameworks are often discussed independently, their overlap can unlock a powerful synergy, enhancing the depth and effectiveness of your business strategy.

The Business Model Canvas, pioneered by Alexander Osterwalder and Yves Pigneur, offers a holistic view of a business model by breaking it down into nine key building blocks: Customer Segments, Value Proposition, Channels, Customer Relationships, Revenue Streams, Key Resources, Key Activities, Key Partnerships, and Cost Structure. This framework serves as a blueprint for understanding how a company intends to create, deliver, and capture value.

The 4Ps framework, introduced by E. Jerome McCarthy, focuses on the essential elements of marketing strategy: Product, Price, Place, and Promotion. It delves into the core components of a marketing plan, guiding businesses in crafting strategies to effectively market their products or services.

While the BMC and the 4Ps might seem distinct at first glance, they converge in several critical areas, particularly concerning product strategy:

-

Product (Part of 4Ps) and Value Proposition (Part of BMC): The product is central to both frameworks. In the 4Ps, product strategy involves decisions regarding product features, branding, and differentiation. Similarly, the Value Proposition block in the BMC encapsulates how a product or service solves a customer's problem or fulfills a need in a unique way. Aligning these two concepts ensures that the product's attributes resonate with the target market's preferences and demands.

-

Price (Part of 4Ps) and Revenue Streams (Part of BMC): Pricing decisions directly impact revenue generation, making the alignment between Price and Revenue Streams crucial. The Price component of the 4Ps framework guides entrepreneurs in setting optimal pricing strategies, considering factors such as costs, competition, and perceived value. Correspondingly, the Revenue Streams block in the BMC outlines how the company monetizes its value proposition. By harmonizing pricing strategies with revenue models, businesses can ensure profitability while delivering value to customers.

-

Place (Part of 4Ps) and Channels (Part of BMC): Place, in the context of the 4Ps, refers to the distribution channels through which products reach consumers. Channels, a key element of the BMC, delineate how a company delivers its value proposition to customers. Integrating these concepts involves selecting the most suitable distribution channels to reach target customers efficiently. Whether through direct sales, online platforms, or intermediaries, aligning Place with Channels optimizes the product's accessibility and enhances the overall customer experience.

-

Promotion (Part of 4Ps) and Customer Relationships (Part of BMC): Promotion encompasses marketing communications activities aimed at raising awareness and driving sales. On the BMC, Customer Relationships elucidate how a company interacts with its customers to cultivate loyalty and satisfaction. By aligning promotional efforts with the desired type of customer relationships (e.g., personal assistance, self-service), businesses can tailor their marketing campaigns to effectively engage with their target audience, fostering long-term relationships and brand advocacy.

In essence, while the Business Model Canvas provides a comprehensive framework for mapping out the various components of a business model, the 4Ps framework offers a focused lens on marketing strategy. By recognizing their intersections and aligning the relevant elements, entrepreneurs can craft cohesive and robust business strategies that resonate with customers, drive value creation, and fuel sustainable growth. Embracing this synergy empowers innovators to navigate the complexities of product innovation and entrepreneurship with clarity and purpose.

Categories:

entrepreneurship

innovation

marketing

Posted

by

Thomas Hopper

on

Permanent link for Unveiling the Synergy Between Business Model Canvas and the 4Ps in Product Innovation on March 29, 2024.