Credit Score

What is a credit score?

Think of a credit score as your financial GPA. It is a number that reflects the information in your credit report. The score summarizes your credit history and helps lenders predict how likely it is that you will repay a loan and make payments when they are due. Lenders may use credit scores in deciding whether to grant you credit, what terms you are offered, or the rate you will pay on a loan.

Information used to calculate your credit score can include:

- the number and type of accounts you have (credit cards, auto loans, mortgages, etc.);

- whether you pay your bills on time;

- how much of your available credit you are currently using;

- whether you have any collection actions against you;

- the amount of your outstanding debt; and

- the age of your accounts.

How is a credit score calculated?

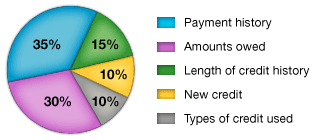

There are many factors that contribute to the calculation of your credit score. The two factors that receive the highest weight in the calculation are your payment history and your debt to limit ratio. It is critical that you pay your bills on time and that you keep your credit card balances low. Although the credit report is free, there is a fee for the credit score, generally less than $10. A credit score is a snapshot in time and may look different at each credit bureau.

How a FICO Score breaks down

Grow Your Credit Score

|

Credit Rating |

Score |

|---|---|

|

Excellent |

730 and up |

|

Above Average |

700-729 |

|

Good |

670-699 |

|

Fair |

585-669 |

|

Poor |

584 or below |

Why is a good credit score Important?

A good credit history increases the confidence of those in a position to loan you money, like lenders and creditors. When they see that you have paid back your loans, lenders are more likely to extend credit again. With good credit, you can borrow for major expenses, such as a car, home, or education. Most importantly you can borrow money at a lower cost.

Generally speaking, the better your credit, the lower the cost of obtaining that credit, usually in the form of interest rates and fees. That means, you'll have more available for savings and spending. Lenders will have more confidence in your ability and commitment to repay the loan on time and in full.

Conversely, if your credit history is not strong, you'll probably pay higher interest rates and fees and have less money available for savings and spending. You could end up being short on money and playing catch-up, juggling between payments on several bills. Over time, higher rates and fees translate into the loss of literally thousands of dollars of potential savings.

For Example:

If you have good credit: A $15,000 car loan at 2% for 4 years costs $325.36 per month for principal and interest. After making all 48 of the payments (12 months times 4 years), the total paid is $15,665.28.

If your credit is impaired: A $15,000 car loan at 16% for 4 years costs $425.10 per month for principal and interest. After making all 48 of the payments (12 months times 4 years), the total paid is $20,404.80.

The difference: That's a difference of $4,739.52 in additional interest you will pay over the life of the 4-year car loan if your credit is impaired and you're charged a higher interest rate on your loan.